The world of taxation is often difficult to understand. It is no different when it comes to furnished rentals. Indeed, owners’ projects are often different in nature, size or duration.

This article is intended to help property owners ensure that your tax return is completed in the most appropriate manner based on your activities in this area. In order to verify your situation and to know the details regarding furnished rentals, we advise you to contact the tax department of your district or, better yet, a chartered accountant specialized in real estate. We would be happy to recommend a trusted professional if you ask us.

The different tax systems

Income from rental activities is systematically considered as industrial and commercial profits (in french “bénéfices industriels et commerciaux” or BIC) and must be declared as such. However, in this large category there are two well-defined systems, each with its own specificities.

The micro-BIC regime

Specifically intended for situations of income below 72 600 €, the micro-BIC regime allows its beneficiary to declare a flat-rate deduction of 50%. You will therefore only be taxed on half of your rental income.

In return, the tax authorities will consider, as a matter of principle, that the expenses related to your furnished rental activity are limited to this 50% and certain expenses will be excluded such as the property tax, the investment in furniture or even the interests coming from the possible loan to acquire the real estate.

The micro-BIC regime is therefore recommended for cases where the property does not require major renovation investments.

Please note: the flat-rate deduction can be as high as 71% when the property is classified as furnished for tourism (“meublé de tourisme”). Moreover, the micro-BIC threshold is 176 200 € and no longer 72 600 €.

The régime réel

The régime réel, as its name indicates, works in such a way that every euro spent on expenses must be counted. The following are considered as expenses directly related to your rental activity

- interest from a loan

- possible repairs/renovations

- the investment linked to the acquisition of the property

- property tax

- investments in depreciable furniture

- co-ownership fees

- insurance against unpaid rent

- etc

In addition, it is also possible to amortize the initial value of the property. Even though the property will tend to increase in value over the years (especially in Paris) rather than decrease in value, from a tax point of view you will be allowed to deduct a small part of the value of the property each year due to its regular use for business purposes.

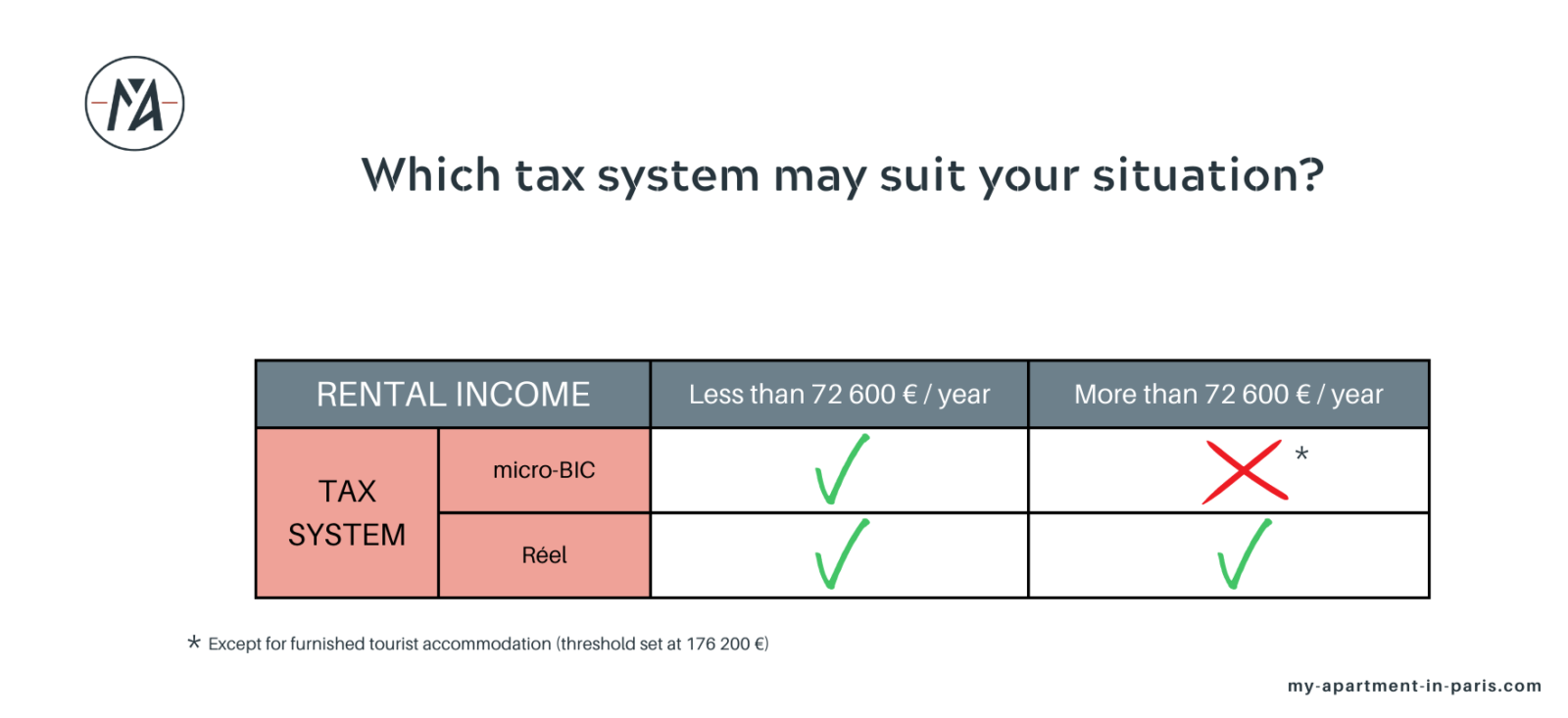

Which tax system should you adopt for your rental activities?

Your rental income is less than 72 600 € per year

If your rental income does not exceed 72 600 € including taxes (expenses included), you will be eligible for the micro-BIC regime (Industrial and Commercial Profits) but you can also choose the régime réel, depending on what best suits your needs.

Your rental income is higher than 72 600 € per year

If on the other hand your rental income exceeds the amount of 72 600 € including VAT, your tax regime will automatically be the régime réel.

The different statuses of furnished renters

LMNP (loueur en meublé non professionnel): non-professional furnished renter

The status of non-professional furnished renter is intended for people whose activity in real estate rental is considered as secondary because it is not the main source of income for their tax household. In any case, it is necessary to carry out a certain number of steps.

Regardless of the status, the first step is to declare your furnished rental activity to the CFE (Centre des Formalités des Entreprises) within 15 days following the beginning of the first rental. To do so, you just have to fill in the Cerfa 11921*07 form. Following this, a SIRET number corresponding to your apartment will be sent to you. If you have several properties to rent, it is essential to repeat this step as many times as necessary.

LMP (loueur en meublé professionnel): professional furnished renter

Unlike the LMNP, the LMP status is intended for people whose rental is considered to be the owner’s main professional activity, especially since most of the tax household’s income comes from this activity. Whatever your profession, it makes no difference to the tax authorities: if more than 50% of your income (out of the sum of your professional income and rental income) is related to furnished rentals (and if it exceeds €23,000), you are de facto considered a real estate professional.

The tax advantages of the LMP status are quite significant. First of all, it allows you to deduct the deficits linked to the rental activity from the global income of the tax household and thus to reduce the taxable income.

In addition, it offers an exemption on the IFI (Impôt sur la Fortune Immobilière) introduced on January 1, 2018 and concerning real estate whose total value exceeds 1.3 million euros.

Similarly, a partial (in the case of revenues between 90,000 and 126,000 euros) or total (revenues below 90,000 euros) exemption from the tax on professional capital gains is granted when one has LMP status. However, you must prove that you have been carrying out this activity for a minimum of five years.

The status of LMP does not change the possibility of depreciation of the real estate which remains accessible on the condition of being under the régime réel and not in micro-BIC.

In return, the persons having this status must pay the contributions of the SSI (Social Security of the Independents) equivalent to approximately 40% of the net profit of the rental activity.

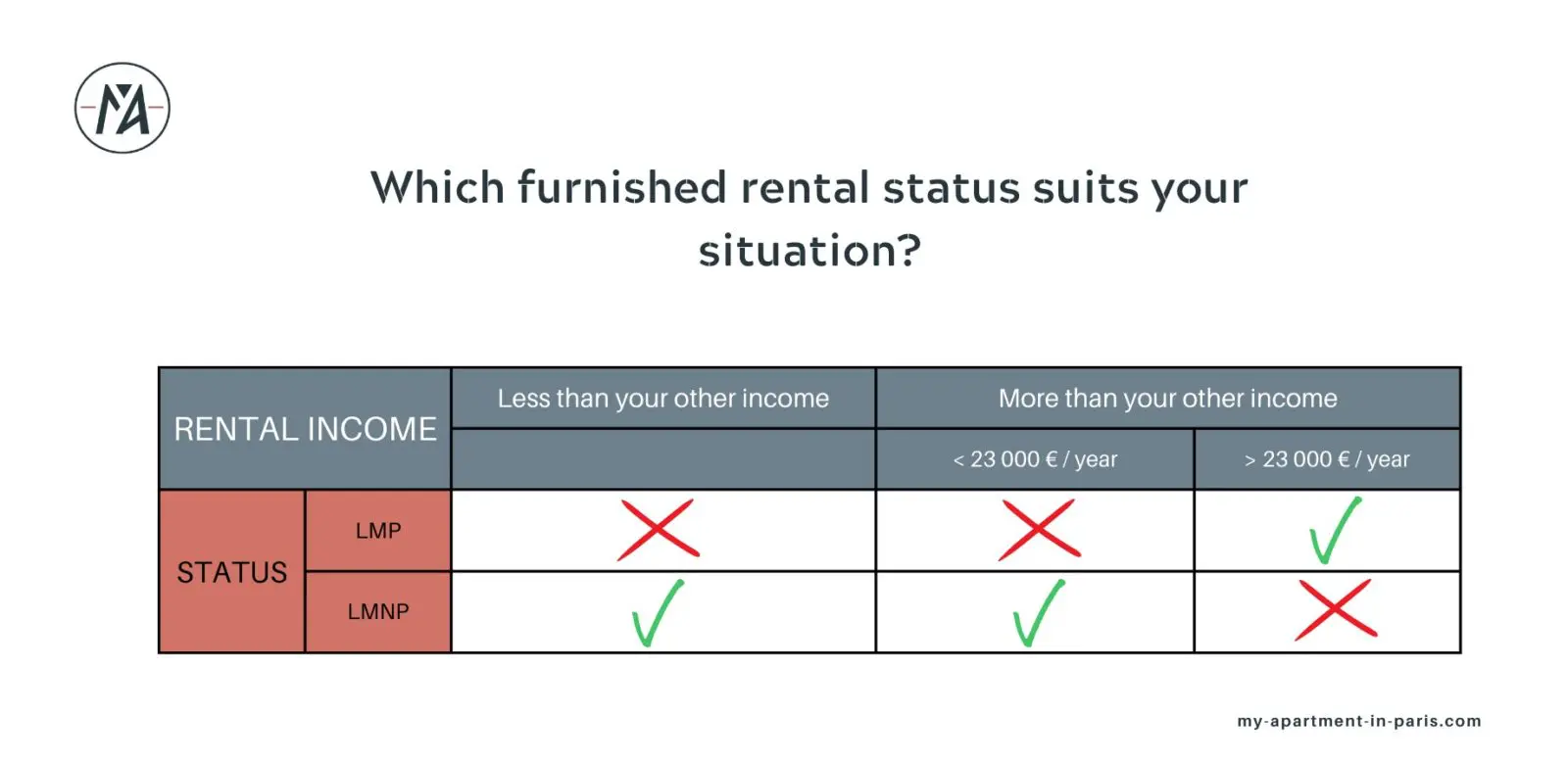

Which status corresponds to your activity?

Your rental income is lower than your other income

Whatever the sum of your rental income, if it does not constitute your main source of income ( meaning professional income, i.e. salaries and benefits), you will automatically be considered as a non-professional furnished renter (LMNP).

Your rental income is higher than your other income

Your rental income is less than 23 000 € per year

If the annual sum of your income from the rental of your real estate is less than 23 000 € including taxes ( expenses included), then you will also have a status of non-professional furnished renter (LMNP).

Your rental income is more than 23 000 € per year

If your income from the rental of your property is higher than 23 000 € including taxes ( expenses included) and if it is higher than your income from a professional activity (salaries and wages), you will obtain the status of professional furnished renter (LMP).

Conclusion

As we saw, the statutes of furnished renter, just like the tax systems, are quite specific. There is not necessarily one better than the other in an absolute sense. They correspond to distinct needs, each case being different from the other (apartment already renovated or not, desire to create a real rental profitability or simply an additional income, etc.). Therefore we can only advise you, after this reading, to call upon a tax advisor before declaring your income, he/she will guide you towards the most relevant choice in relation to your situation.